The Domino Effects of Costlier Debt: Impacts on Leveraged Finance and M&A

The Bank of England has just raised interest rates for the 13th consecutive time following data which shows inflation remained stuck at 8.7% in May. The Bank’s Monetary Policy Committee – the body responsible for deliberating on the benchmark rate – voted seven to two for a half-point increase to 5.00%. Almost all major central banks have adopted similar rates. This article will explore the ramifications of increasingly costlier debt, beginning with an analysis of the low-cost debt conditions during the 2010s then comparing those conditions with the current environment.

2009-2021 – An ‘Era of Free Money’

In March 2009, for the first time since the financial crisis, UK interest rates dropped below 1.00%. What ensued was a decade of cheap borrowing. This created a deal-favourable environment, in which mergers and acquisitions (M&A) activity hit all-time highs repeatedly throughout the 2010s. A key driver of this was the rapid growth of private equity. Private equity houses buy and sell companies for profit, and they finance acquisitions through a combination of equity (contributed by investors) and debt (loans and bonds). Loans and bonds carried low-interest rates, allowing the proportion of borrowed funds used to finance acquisitions (leverage) to increase. Leveraged buyouts (LBOs), where the ratio of borrowed funds is often 90% to 10% equity, made larger and more profitable deals more attainable. Market liquidity made exit opportunities plentiful, enabling returns to be realised easily and contributing to a high deal turnover. The net effect was a flourishing private equity industry, with transactions increasing from $93bn/year in 2009 to $1.012tn/year in 2021 (Statista). The advisors of private equity houses – big banks, law firms, consultancy firms, and others – reaped substantial profits.

2022-Present – The End of Free Money?

During 2022, almost all major central banks adopted high-interest rates to combat inflation. Current inflation is a product of upward price movements of food, drink, energy, durables, and transportation. The war in Ukraine and supply chain bottlenecks have reduced the supply of many raw materials and goods. Per the law of supply and demand, increased scarcity has had the broad effect of price hikes. By raising rates, central banks increase the cost of borrowing, which reduces the amount of money people and businesses can spend; this helps reduce the demand for goods and services, thereby bringing prices down.

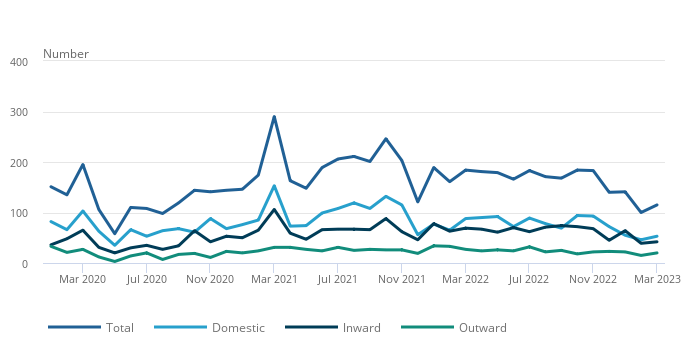

In periods of high-interest rates, M&A suffers: this year, global M&A activity had its slowest start in a decade, with a 45% year-on-year decline in deal value during Q1. Higher rates lead lenders to tighten their financing terms, reducing access to capital; furthermore, higher rates being factored into valuation models can result in lower valuations for target companies, making them less attractive to potential acquirers. But the main reason for the slump in M&A is the increased cost of debt – loans, bonds, and other debt instruments carry higher interest rates, making them more costly to use in acquisition finance. In a survey of UK CFOs published in January, Deloitte found that debt finance is the least attractive since the financial crisis. Total M&A activity involving UK companies fell from 290 in March 2021 to 115 in March 2023 (see Figure 1).

Figure 1. Source: Office of National Statistics

Trends in Debt Finance

Two products are used primarily in the debt portion of LBOs: bonds and loans. Bonds, in particular, are a disfavoured means of financing currently. High-interest rates drive the price of bonds on the secondary market down. Consequently, their coupon (interest) rates increase relative to their trading price, increasing their yield. When bonds already trading have high yields (and so offer high returns to investors), it becomes harder for new bond issuances to attract investors with lower coupon rates. Issuers would need to match market yields, which are high and costly.

Baker McKenzie, in its annual report on leveraged finance, notes a shift away from bond markets in favour of bank finance to make up the debt portion of buyouts. Bank finance involves obtaining loans and credit facilities from financial institutions. Loans and credit facilities are generally more flexible than bonds, allowing more leeway on repayment schedules, interest rates, and covenants; they are also less reliant on market conditions. Often structured as senior debt within the capital structure, they offer lenders more security and lower risk.

Within bank finance, pro rata loan facilities have risen in prominence. Pro rata debt is typically held by banks and financial institutions until maturity. Each lender holds a share proportionate to their participation in the financing. It often has a fixed repayment schedule, a low-interest rate, and is covenant-heavy. Pro rata debt is typically categorized as part of the private credit market since it involves direct lending arrangements between borrowers and a group of lenders, rather than being publicly traded. These traits make it a more stable and resilient form of financing than institutional loans.

Institutional loans are usually split into tranches, each with its own terms and conditions. Tranches are sold to different investors on the secondary market (a process called syndication), which diversifies risk. But amid current market volatility, it is proving challenging for arrangers to sell all the tranches. Bids for tranches have fallen substantially, forcing lenders to retain committed finance for LBOs on their books or discount it at a loss. A notable example is the financing provided for Elon Musk’s acquisition of Twitter, where arrangers lent $12.7 billion. Due to prevailing market conditions, they faced difficulty selling a significant portion of the debt, forcing them to retain unsold tranches and incur losses. In H1 2022, 67% of leveraged loan issuance in the US comprised pro rata tranches.

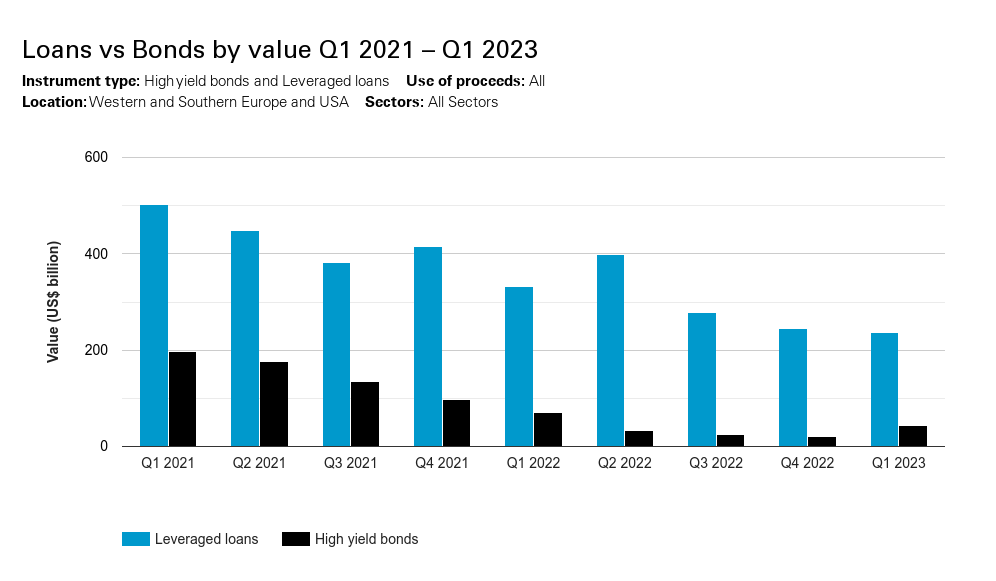

Figure 2. Source: White & Case’s Debt Explorer

The Future of Debt Finance and M&A

As long as interest rates remain high, debt finance will continue to be costly. Loans are increasingly favoured over bonds, and among loans, there is a growing preference for privately negotiated, direct-lending facilities that are not traded on the secondary market. These debt structures reduce risk and provide security to lenders while also maintaining a cost-effective capital structure for LBOs.

But M&A activity is only likely to make a full recovery when interest rates fall to lower levels. Advisors are starting to feel the effects of the deal drought – law firm Orrick, Herrington & Sutcliffe just announced a 6% reduction of its workforce. This follows a series of BigLaw layoffs, notably by firms servicing private equity clients. The layoffs reflect a wider trend throughout the professional services industry.

Unfortunately, interest rates are likely to fall slower than previously expected. Recent data show that UK wage growth climbed by 7.6% in Q1 of this year. When wages increase, the general effect is an increase in prices, keeping inflation up. Markets predict that the Monetary Policy Committee will raise rates to 5.76% by the end of 2023, which would see deal activity contract further.

By

Joshua Troup