When Banks Fail: Analysing Credit Suisse's Downfall and the Potential Legal Impacts

Source: Credit Suisse

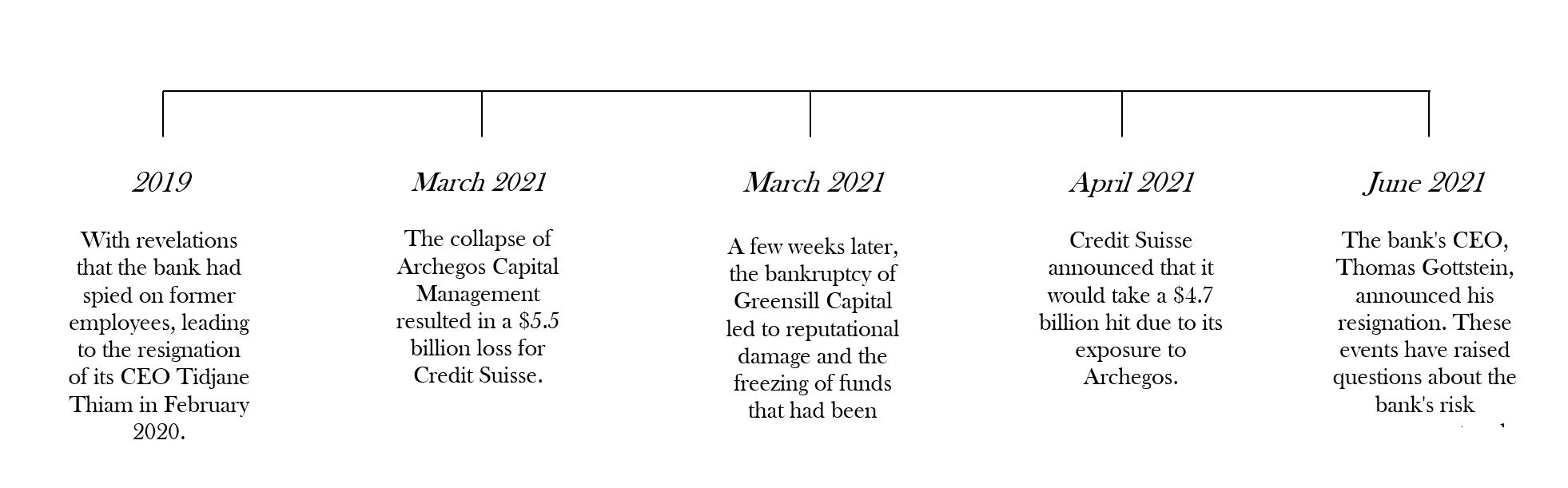

Credit Suisse, a prominent Swiss bank, has been through a whirlwind of trouble lately, causing major concern for investors and the banking industry as a whole. With a history spanning over 160 years, the bank has recently suffered significant financial and reputational losses, leading to a 24% drop in share price, a mass exodus of clients, and a slew of issues raised in its financial report. This article delves into the timeline of events, Credit Suisse's current actions, and the response from investors, and explores the implications of this turmoil for the Swiss banking industry and beyond.

With a presence in over 50 countries and a workforce of approximately 50,000 employees, the bank has built a reputation for providing exceptional financial solutions to its clients. Credit Suisse offers a range of services including investment banking, private banking, asset management, and retail banking, catering to clients worldwide. Despite its impressive track record, Credit Suisse has faced significant challenges in recent years, including a series of scandals that have impacted its reputation and financial performance. This is the timeline of the events:

Let's delve into the notorious collapses of Archegos Capital Management and Greensill Capital. Archegos Capital Management is a family office hedge fund. Credit Suisse was one of the prime brokers for Archegos and ended up losing $5.5 billion due to its exposure to the fund's risky bets. Another contributing factor was the bankruptcy of Greensill Capital, a supply chain finance company, in March 2021. Credit Suisse had invested heavily in Greensill and had to freeze funds that it had promoted as low risk, resulting in reputational damage. The bank's risk management has also come under scrutiny, with some analysts questioning whether it adequately assessed the risks associated with its dealings with Archegos and Greensill.

In addition to these significant losses, Credit Suisse has also faced regulatory scrutiny and fines, including a $4.7 billion settlement with the US Department of Justice related to its role in the 2008 financial crisis. Credit Suisse is taking several actions in response to its recent troubles. The bank has announced plans to reduce risk and cut costs, including a reduction in the size of its investment banking division by around 30%. The bank's CEO, Thomas Gottstein, has acknowledged that the bank's risk management system needs improvement and has vowed to make changes. Credit Suisse has announced a plan to reduce risk-weighted assets by $35 billion over the next two years to address these issues. While these actions are a step in the right direction, they may not be enough to restore the bank's reputation and regain investor trust.

Credit Suisse's recent troubles have not gone unnoticed by its biggest investors, who have raised concerns about the bank's financial health and stability. One of the biggest blows came from Harris Associates, which holds a 3.1% stake in Credit Suisse. In April 2021, the investment firm announced that it could not further help the bank. The Qatar Investment Authority, which holds a 5.2% stake in Credit Suisse, has also expressed concerns and reportedly sought reassurances from the bank's management. Additionally, Norges Bank, which manages Norway's sovereign wealth fund and holds a 3.5% stake in Credit Suisse, has been critical of the bank's risk management practices. In May 2021, Norges Bank reportedly criticized Credit Suisse's board for failing to address concerns about the bank's exposure to Archegos Capital Management. Other major investors, including those from Saudi Arabia, Singapore, and Sweden, have also been selling off their Credit Suisse shares in response to the bank's troubles. The bank's finance report has also raised red flags, with the report stating that "the Bank may incur significant losses in connection with certain significant clients" and that "there can be no assurance that such losses will not exceed the Bank's current expectations." These concerns have been reflected in Credit Suisse's share price, which has been steadily declining. As the bank continues to grapple with its challenges, its relationship with these investors is likely to remain a key factor in its recovery efforts.

In a shocking move to avoid a financial meltdown, Credit Suisse has been snatched up by its arch-nemesis UBS in a bargain deal. With just hours to spare before the opening of financial markets, the 167-year-old lender, which was once worth over £65bn, was acquired for a measly £2.6bn. Rival banks were frantically preparing for a possible contagion across the entire European banking sector over the weekend, despite official assurances that everything was under control. The merger between Credit Suisse and UBS is set to cause major job losses in the UK, while the bank's Asian operations seem to be holding steady. The rescue of Credit Suisse is bound to put pressure on the Bank of England to hold off on interest rate hikes at their next meeting, as such increases could put additional strain on weaker lenders. But the Swiss finance minister isn't taking any chances, warning that the failure of Credit Suisse could lead to "irreparable economic turmoil in Switzerland and beyond." Officials from Switzerland, the UK, and the US have been working together to prevent such a catastrophe.

The story of Credit Suisse's fall is nothing short of a cautionary tale of what can happen when banks get it wrong. With the bank facing a host of troubles - from financial losses to regulatory scrutiny and the loss of clients - the situation has snowballed into a full-blown crisis. While Credit Suisse attempts to limit the damage, it's clear that the legal ramifications of the bank's failures are going to reverberate through the industry for a long time to come.

By

Sujatha Baskaran